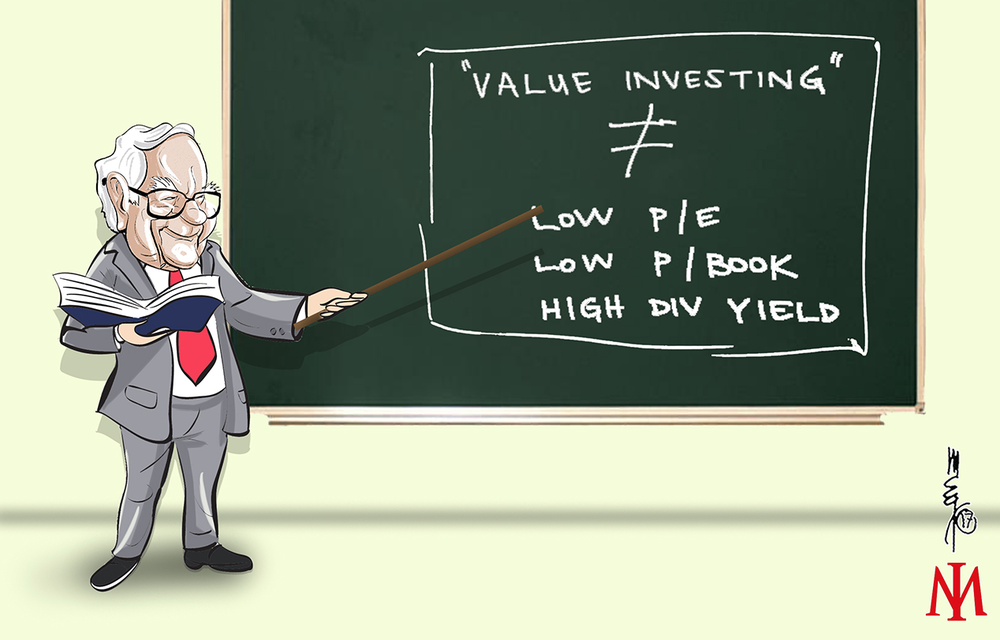

Different sources define value investing differently. Some say value investing is the investment philosophy that favors the purchase of stocks that are currently selling at low price-to-book ratios and have high dividend yields. Others say value investing is all about buying stocks with low P/E ratios. You will even sometimes hear that value investing has more to do with the balance sheet than the income statement. In his 1992 letter to Berkshire Hathaway shareholders, Warren Buffet wrote:We think the very term “value investing” is redundant. What is “investing” if it is not the act of seeking value at least sufficient to justify the amount paid? Consciously paying more for a stock than its calculated value – in the hope that it can soon be sold for a still-higher price – should be labeled speculation (which is neither illegal, immoral nor – in our view – financially fattening).Whether appropriate or not, the term “value investing” is widely used. Typically, it connotes the purchase of stocks having attributes such as a low ratio of price to book value, a low price-earnings ratio, or a high dividend yield. Unfortunately, such characteristics, even if they appear in combination, are far from determinative as to whether an investor is indeed buying something for what it is worth and is therefore truly operating on the principle of obtaining value in his investments. Correspondingly, opposite characteristics – a high ratio of price to book value, a high price-earnings ratio, and a low dividend yield – are in no way inconsistent with a “value” purchase.Buffett’s definition of “investing” is the best definition of value investing there is. Value investing is purchasing a stock for less than its calculated value.Tenets of Value Investing1) Each share of stock is an ownership interest in the underlying business. A stock is not simply a piece of paper that can be sold at a higher price on some future date. Stocks represent more than just the right to receive future cash distributions from the business. Economically, each share is an undivided interest in all corporate assets (both tangible and intangible) – and ought to be valued as such.2) A stock has an intrinsic value. A stock’s intrinsic value is derived from the economic value of the underlying business.3) The stock market is inefficient. Value investors do not subscribe to the Efficient Market Hypothesis. They believe shares frequently trade hands at prices above or below their intrinsic values. Occasionally, the difference between the market price of a share and the intrinsic value of that share is wide enough to permit profitable investments. Benjamin Graham, the father of value investing, explained the stock market’s inefficiency by employing a metaphor. His Mr. Market metaphor is still referenced by value investors today:Imagine that in some private business you own a small share that cost you $1,000. One of your partners, named Mr. Market, is very obliging indeed. Every day he tells you what he thinks your interest is worth and furthermore offers either to buy you out or sell you an additional interest on that basis. Sometimes his idea of value appears plausible and justified by business developments and prospects as you know them. Often, on the other hand, Mr. Market lets his enthusiasm or his fears run away with him, and the value he proposes seems to you a little short of silly.4) Investing is most intelligent when it is most businesslike. This is a quote from Benjamin Graham’s “The Intelligent Investor”. Warren Buffett believes it is the single most important investing lesson he was ever taught. Investors ought to treat investing with the seriousness and studiousness they treat their chosen profession. An investor should treat the shares he buys and sells as a shopkeeper would treat the merchandise he deals in. He must not make commitments where his knowledge of the “merchandise” is inadequate. Furthermore, he must not engage in any investment operation unless “a reliable calculation shows that it has a fair chance to yield a reasonable profit”.

5) A true investment requires a margin of safety. A margin of safety may be provided by a firm’s working capital position, past earnings performance, land assets, economic goodwill, or (most commonly) a combination of some or all of the above. The margin of safety is manifested in the difference between the quoted price and the intrinsic value of the business. It absorbs all the damage caused by the investor’s inevitable miscalculations. For this reason, the margin of safety must be as wide as we humans are stupid (which is to say it ought to be a veritable chasm). Buying dollar bills for ninety-five cents only works if you know what you’re doing; buying dollar bills for forty-five cents is likely to prove profitable even for mere mortals like us.